The Student Loan System is Dead. The Pandemic Killed It.

Defenders of the federal student loan program are extremely worried. They are trying very hard to turn the federal student loan system back on, so far unsuccessfully , at least until May 1st of next year.

In recent weeks- and in the coming months, we’ve seen and we’ll see a flurry of articles attempting to force a “smooth transition” (Jen Psaki’s words) back into loan repayment after a nearly two-year pause. Some, like Mark Kantrowitz, are arguing that there will be no student loan “apocalypse” when payments resume. Others, like Beth Akers, are making increasingly bizarre arguments that resuming payments will actually combat tuition inflation.

These pieces are, and will be loaded with accusational rhetoric disguised as “helpful advice” (this is an old, long-used banker’s trick designed to blame the borrowers for this problem). One example (Kantrowitz):

“…If a borrower’s spending increased during the pandemic, they should review their budgets to free up money to start making student loan payments. Cut back on discretionary expenses. Borrowers can also increase their income by asking for a raise, working a part-time job in the evening and weekends, or by switching to a better-paying job.”

Of the thousands of accounts I’ve received over the past 2 years from people who’ve lost jobs, been evicted, had their hours cut, their rents jacked, their purchasing power slashed by inflation, etc, I can’t recall a single report of Covid-induced-splurging. I suspect that is a phenomenon that exists only in the imagination of student loan swamp minions, or perhaps among the fortunate millionaires and billionaires who actually managed to profit from the pandemic. Not the student loan borrowers.

This is getting ridiculous.

The increasing desperation- and sheer volume- of these articles betray a fact that everyone who knows- and especially those who defend- the federal loan program realize, but few possess the intellectual honesty to admit:

The student loan “apocalypse” has already happened- more than two years ago. The pandemic is the nail in it’s coffin. There is no saving it, and there is no good reason to save it.

Before the pandemic, the Brookings Institute estimated that student loan defaults for the Class of 2004 would reach 40%. This is more than double the default rate for subprime home mortgages of less than 20%. These borrowers, however, were borrowing less than a third (roughly $13,000) of what is borrowed today (roughly $39,000). Wages have not tripled since 2004. They have flatlined with inflation, at best. Given this, it should not be controversial to say that defaults for all current student loan borrowers were going to be at least 60–70% (if not higher)…before the pandemic.

In 2019, Education Secretary Betsy DeVos acknowledged that 75% of all federal student loan borrowers were “unable to pay down their loans”. Wayne Johnson, the Federal Student Aid Director, said that this was closer to 80% in the first months of 2020. Department of Education data for that time period shows that more than half of all borrowers weren’t paying at all.

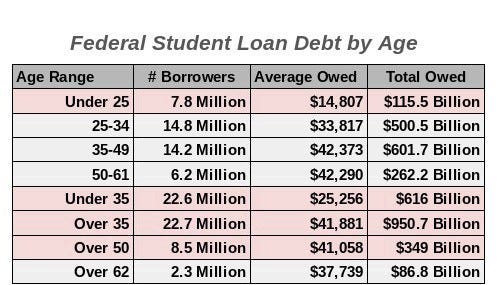

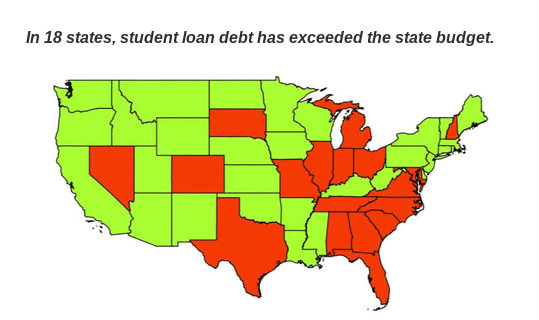

This is also not a younger person’s problem anymore: More than half of all borrowers are now over 35 years old, not under 35. People over 50 with student loans now outnumber people under 25. For both of the older groups, they owe far more than their younger counterparts, despite having borrowed far less many years or decades ago. Equally disturbing: student loan debt in over a third of U.S. States now exceeds their state budgets.

A default rate 3–4 times higher than the subprime rate. Fewer than half of all borrowers paying. 80% of all borrowers underwater. Older borrowers outnumbering younger borrowers, and owing far more despite having borrowed far less. All of these happening before the pandemic. Is this not indisputable evidence of a totally and catastrophically failed lending system?

The 45 million borrowers have obviously inculcated this. They have had a chance to reflect on the debt. They’ve seen trillions in economic stimulus (including $1 Trillion in PPP loans that don’t need to be repaid)thrown out to the country. Much of this stimulus has gone to millionaires, billionaires, and even colleges, who have never been in a stronger financial position than they are right now. All of these giveaways added to the national debt, and required money to be printed, or drawn from the Treasury. Federal student loans, on the other hand, can be cancelled without drawing even a penny from the Treasury or adding even a dime to the national debt.

Incidentally, “Student Loan Voters” represent, by far, the largest untethered voting bloc in modern American politics. The Biden campaign managed to temporarily win their votes in the 2020 Presidential election by promising to both return bankruptcy protections, and “eliminate” federal student loan debt for public college/HBCU borrowers earning less than $125k/year, but this allegiance has all but evaporated in view of his blatant betrayal of these voters in the days and months after his election.

The people have come to understand this, whether intellectually, or just viscerally. Most weren’t paying before the pandemic, almost none are paying at the present time, and when (if) the Biden Administration gathers the nerve to attempt to turn this failed, rigormortised lending system back on, it would be surprising if even 25% were paying a few months after they flip the switch.

Frankly, they shouldn’t pay. Conservative Grover Norquist once said that government should be small enough that if needed, it could be “taken to the bath, and drowned in the tub”. This is precisely what is needed for this lending beast. It should not be fed. It should be starved, and that is what is happening.

Federal student loans are, for better or worse, vanishing into a mist of illegitimacy, and time only hardens this popular rejection. There is literally nothing that can be done to change this fact.

Lending systems fail from time to time. This has been true dating back to biblical times, and continues to be true to the present day. In the mid-eighties, for example, the S&L crisis saw the failure of a third of U.S. Savings and Loan Institutions, and the dissolution of the Federal Savings and Loan Insurance Corporation (FSLIC). More recently, the aforementioned Subprime Mortgage Crisis nearly took down the entire world economy.

Removing bankruptcy protections (and other consumer protections) uniquely from student loans lies at the core of the current catastrophe, and is what differentiates it from the S&L and sub-prime failures. There is a good reason the Founders called for uniform bankruptcy laws ahead of the power to raise an army and declare war in the U.S. Constitution, and this craven, cruel violation of the spirit (and letter) of the law proves their wisdom in spades. While stripping bankruptcy away uniquely from student loans may have possibly served to compel repayment in year’s past, that utility is now gone. The people have spoken, and will speak much louder in the coming months: The lending system is finished.

Biden would do well to immediately order the Department of Education to stop opposing student loan borrowers in bankruptcy proceedings. Congress would do well to immediately pass S.2598, a bipartisan bill that will return bankruptcy rights to federal student loans, and compel modest repayment from the colleges when loans are discharged. At this late date, however, it really is easier, cheaper, and far more stimulative to simply cancel all of the loans, call it stimulus, and start from scratch.

President Biden can spend the next 3 years pretending that the federal student loan system is viable, and preside over a painful, messy, probably civilly-unrestful unwinding. Or, he can toss this train wreck on the scrapheap of failed U.S. policy experiments, and spend (possibly) the next 7 years creating an efficient, fair, and uncorrupted higher education financing system that actually works.

Pretty easy choice, one would hope.