All of the Department of Education’s Income-Driven Repayment Programs are Cruel Jokes.

Both current and proposed IDR programs are not to be trusted in the continued absence of standard bankruptcy protections.

Updated 12/23/2023

Since 1995, a confusing array of Income-Driven Repayment programs (IDRs) have been foisted on the public by the Department of Education for federal student loans, each promising to cancel student loan debt after borrowers pay based upon their incomes for varying time periods. These include Income Contingent Repayment (ICR), Income Based Repayment (IBR), Pay-As-You-Earn (PAYE), and Revised Pay-As-You-Earn (REPAYE). The Public Service Loan Forgiveness Program (PSLF), while not technically a repayment program, is also mixed into this alphabet soup.

Confused yet? It gets better. There is also President Biden’s proposed IDR, which “amends the terms of the Revised Pay-As-You-Earn plan”. So hilariously, we now even have a “Revised,Revised Pay-As-You-Earn” program, mercifully re-dubbed as The SAVE Plan, about to be thrown on the pile.

Reader: Do not be afraid! I will not abuse you by taking you through these programs in detail. I’ll leave that to the legions of “student loan lawyers”, student debt coaches, counselors, and other predators who profit (at the borrowers expense) by baffling and bamboozling vulnerable and desperate borrowers into loan rehabilitation, consolidations with the carrot of what these IDR plans promise as bait.

Thankfully, there is no need to, because these plans all share a common characteristic that make further analysis unnecessary:

All of these IDR’s are being run by a Department of Education which has no desires or intentions of cancelling any loans. The vast majority of borrowers are being expelled from the programs, and will not only not be getting the loan cancellation promised; they will be left owing far more than had they never tried in the first place.

The Chronicle of Higher Education reported in 2015 that 57% of those enrolled in IDR programs had been disqualified in one year alone for failure to “verify their income”, an annual, onerous exercise required of the borrowers- and one of many ways the Department has to disqualify people out of the programs. Given that around 30% of these income verification forms are rejected in a typical year, simple calculation shows that the probability of making it through 20 consecutive years shrinks to 0.08%- a vanishingly small percentage. This goes even lower for 25 year terms.

Also: of millions of people who enrolled in the Income Contingent Repayment Program (ICR) since 1995, only 32 people had made it through as of 2021.

For the Public Service Loan Forgiveness Program (PSLF), the disqualification rate was 99% as of 2018. It remains to be seen what results an “overhauled” version of this plan (introduced only because of fierce public outcry from various unions) will yield, but the recent announcement of 800,000 new approvals doesn’t count all the people who have fallen out of people in year’s past, and didn’t even apply, so that only a tiny fraction of those who tried for this program will get the promised relief. And as the chart below shows, these, and other cancellation are very small drop in the bucket.

A cruel irony: Most people enrolled in IDR’s have increasing loan balances throughout the term of their repayment. When they are disqualified out of these programs, they are usually left owing a far larger balance than had they never tried in the first place. At least on the books- the Department of Education is almost surely booking a profit rather than incurring a cost due to these non-functioning IDR plans. The cost and harm that these failing IDR’s have caused the citizenry has been incalculably large.

Not to mention, these programs are all very vulnerable to political changes. They could all be ended tomorrow if Congress decided to end them, and many (mostly Republican) lawmakers have expressed a strong desire to do just that for many years.

Here is the big-picture on Biden’s student loan cancellation in the first 3 years of his Presidency:

While the claimed $131 billion in loan cancellation may sound like a significant amount, this was over a 3 year time span, during which the federal loan portfolio (but for the pandemic interest pause) typically grows by $300 billion in interest, alone.

So, Biden could do similar loan cancellations forever, and with new loan originations, the federal student loan portfolio would still grow by about $1.6 Trillion over ten years (actually significantly more than this, when capitalized interest is considered).

The Department of Education clearly has no desires or intentions of actually cancelling any loans if a reason can be found not to, and this has always been true. The bad faith with which the Department runs this lending program has been obvious for decades. Since the constitutional right of bankruptcy protections was stripped uniquely from the loans, they have become increasingly predatory, and the institutional culture of administering the loans with an eye towards disqualifying as many borrowers out of the IDR’s as possible has only become more vicious and blatant.

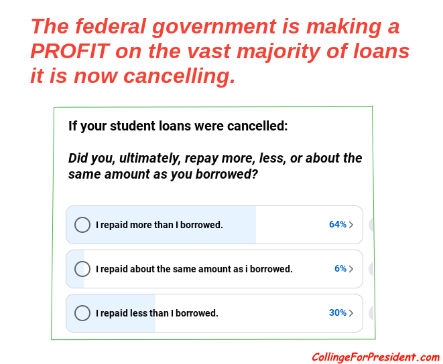

Interestingly: we did a survey of a relatively small number of our members who have been lucky enough to finally get their loans cancelled. We found that the large majority of them, ultimately, repaid more- often far more- than they had originally borrowed. This indicates strongly that even on the few loans that are currently being cancelled, the Department of Education has obviously made a significant profit, has not incurred a loss:

Make no mistake: The Department fights tooth-and-nail behind the scenes to keep constitutional bankruptcy rights away from the loans, and this has not changed with the “new” bankruptcy process announced last year. As long as this vital protection remains gone, the un-elected, unappointed bureaucrats there will continue to abuse the borrowers, extract obscene- and ever-increasing amounts of unearned profit from them.

This never-ending parade of designed-to-fail IDR’s only perpetuates this unconstitutional, catastrophically failed loan scam into the future, and quite frankly, looks very much like indentured servitude at this point, which, along with slavery, was outlawed in 1865.

Student loan borrowers should not be fooled. They should be demanding the return of constitutional bankruptcy rights to the debt. Frankly, they should not feel obligated to pay on their student loans unless/until this constitutional right is returned to them.

Frankly, however, the lending system is so failed at this point, the loans probably should be cancelled entirely, for the good of the country, and a fairer, less costly and damaging model for educating the citizens should be put in it’s place. This will be needed for economic stimulus going forward anyhow, and unlike PPP Loans, will require nothing from the Treasury, and will add nothing to the national debt.

If you agree, sign and share this petition.