Astroturf has Overrun Student Loan Activism.

I am the first activist in the country on the student loan issue and founded the first grassroots group dedicated to fighting for student loan justice. I wrote the first book to be critical of the American student loan system and wrote the petition in early 2020 that launched the concept of cancelling student loans by executive order into the national conversation, and made it into the viable issue that it has become.

I’ve been doing this for 20 years, at great personal cost, sacrifice, and austerity. And I’ve done it honestly, always and only fighting for the borrowers, never doing deals with the student loan industry, despite being presented with many opportunities to do so.

Over these years I’ve seen all manner of grifters, charlatans, and opportunists come onto the scene. Most are simply trying to make easy money, selling pyramid schemes, promising instant debt relief, or other tonics. They pop up like mushrooms after a rain, and are usually gone again about as quickly. They are obvious, obnoxious, and pretty easy to spot.

But there is another, far more dangerous/insidious class of operatives who have entered the student loan space for nefarious purposes: Corrupted groups pretending to be fighting for student loan borrowers in the political sphere, when in fact they are actually serving corporate/lending interests.

AKA: Astroturf.

In December,2005, a leaked, internal strategy memo from Sallie Mae (by far, the largest and most dominant player in the student loan industry at the time) surfaced, and was disseminated to the public. The memo outlined both the company goals and planned strategies. The highest legislative goal was to preserve the bankruptcy exception for private student loans, which the company had won from Congress in the bankruptcy bill of that year a few months earlier. The memo went on to propose a strategy for utilizing social media to sway/push public opinion in ways favorable to their goals.

Much has changed since 2005. The federal government now makes the loans, and total student loan debt, nationally, has exploded. While the cast of players in the student loan industry has changed somewhat, it is clear that the industry goal of keeping bankruptcy gone from student loans, and using social media to change public opinion and influence federal lawmaking towards that end certainly happened, and remains fully intact to this day.

More than a few groups have cropped up since 2007, all claiming to be fighting for student loan borrowers- loan cancellation in particular. They’ve come onto the scene with great fanfare, very sophisticated and well-funded social media infrastructure, and suspiciously wide exposure in news media. They have proceeded to undermine/confuse/distract from the true activists in this arena.

I’ve seen this corruption up close, and witnessed the damage it has wrought, the real harm it has caused millions of people, and the years it has added to the struggle for actual student loan justice.

Below are two examples to consider.

- The Debt Collective.

This group made their debut at Occupy Wall Street in 2011. They claim to be fighting for the cancellation of student loan debt. What the group does, however, is starkly different.

They are, in fact, business partners with the student debt collection industry (ie Wall Street), and have been since their inception (ironically, at Occupy Wall Street). They funnel millions to debt collectors to purchase worthless, private student loans on the market, and claim to be helping people by cancelling them. The loans are, however, well past their statutes of limitations, are legally unenforceable, so that the only people actually benefiting from these transactions are the collection industry who now have a new buyer for their worthless loans, and I presume, The Debt Collective itself.

I tried to warn people about them long ago.

What is most disturbing about this group: The debt collection industry has wanted- more than anything else- to see a mass default on student loans with the right of bankruptcy gone from the debt for decades (bankruptcy rights have been stripped uniquely from student loans). This would be a true feast for the industry. In the absence of bankruptcy rights (as well as statutes of limitations for federal loans), the industry has the predatory muscle to extract vast sums from defaulted borrowers.

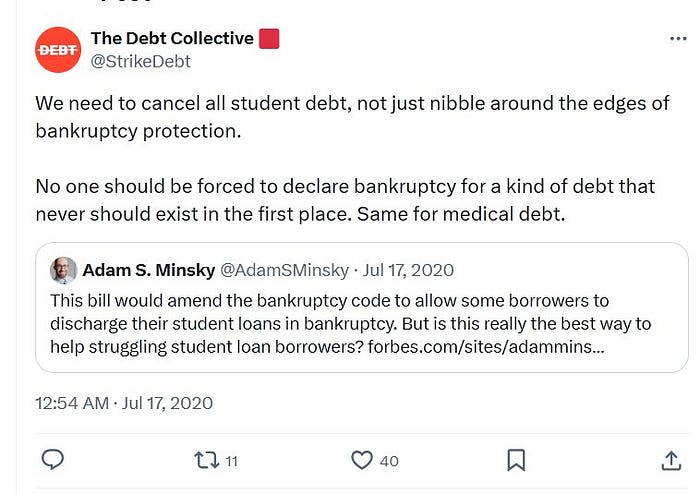

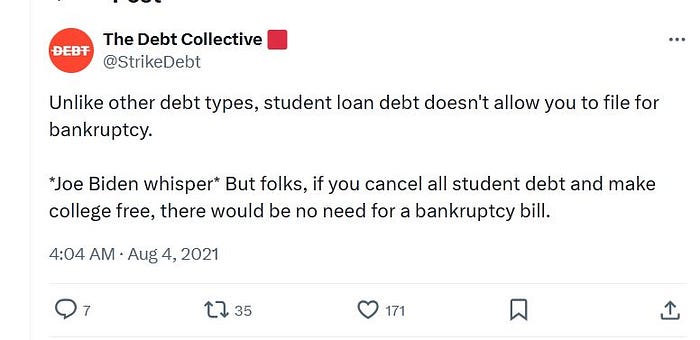

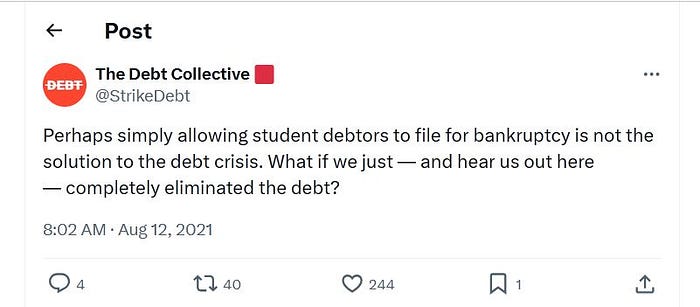

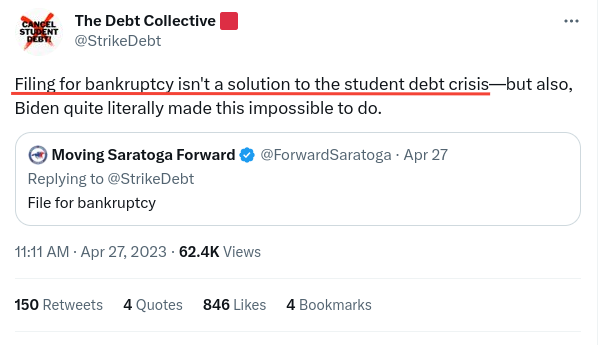

The Debt Collective has been calling for a “Debt Strike” since their inception. They have, however, been almost completely silent on returning bankruptcy rights, and even disparaged it at critical times over the past decades when good bankruptcy bills were in Congress.

Their proponents on social media (usually anonymous twitter accounts) have continuously and consistently argued against returning bankruptcy rights, usually using the argument that bankruptcy is unpleasant.

They never acknowledge that it is the leverage of bankruptcy- without anyone having to file, which will compel all manner of long-overdue relief, including widespread, pre-emptive cancellations, reductions in interest, negotiated settlements, and other fair workouts. And this is without anyone actually having to file.

In fact, it is obvious to anyone studying this issue carefully that we won’t see meaningful loan cancellations, or many/any of the relief measures above unless and until the leverage of bankruptcy rights is restored!

I struggle to raise even $3,000/month from distressed student loan borrowers to fight this battle. I can say with supreme confidence that there is absolutely NO WAY the Debt Collective raises the millions it needs every year for its staff of 25 people, its overhead, etc on donations from distressed student loan borrowers, which requires millions/year. Their funding sources, of course, are secret.

How the debt collection industry makes money:

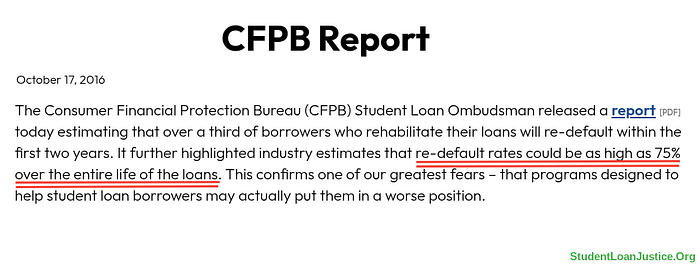

Aside from collecting from defaulted student loan borrowers, the industry can make far, far MORE through a process called “Loan Rehabilitation”, where defaulted borrowers ultimately sign for a new, MUCH LARGER loan, and the agents administering this stand to make a 16% commission on the new, much larger loan.

For example: If a borrower who defaults on a $50,000 federal student loans and signs for a new, $100,000, u defaulted loans, the federal government pays a $16,000 commission. All of this, of course is added to the loans.

The KEY POINT: These “rehabilitated” loans default AGAIN 75% of the time, if not more (Moody’s claimed in 2009 that the re-default rate for rehabilitated loans was 4 times higher than that of normal loans):

The legion of “Student Loan Lawyers”, “Debt Coaches”, “Planners, and others (like Adam S. Minsky, mentioned above) who dupe people into taking these toxic, harmful loans surely NEVER tell their clients the truth about these loans. The fact that they would encourage anyone to take them out in the first place speaks volumes about their ethical and moral bankruptcy. They are setting their own clients up for failure. And they KNOW IT.

The people running this group (Thomas Gokely, Astra Taylor, and others), are not stupid. The debt collection industry people behind them are definitely not stupid. Anyone who studies this issue knows full well the importance of the leverage of bankruptcy rights for compelling any real relief measures for student loan borrowers. They know FULL well that had standard bankruptcy leverage been returned to these loans when they first sold out to Wall Street (at Occupy Wall Street, no less), there would be no crisis today.

Today, with repayment resumed, and the “on-ramp to repayment” expired, the collection industry’s “Golden Fantasy” is about to come true. Bankruptcy rights remain gone from the loans, there is now an unstoppable mass default underway, and the Debt Collective’s partners are about to have a feast at the expense of Debt Collective’s own members.

A quick story from the day of their inception at Occupy Wall Street.

In 2011, I lived at Occupy Wall Street in Manhattan for 2 1/2 months. One day, I saw two student loan collection industry representatives, Jerry Ashton and Craig Antico, at the park. They approached me. This was The ONE DAY that the Debt Collective showed up make their big splash in the media with a stage, T-shirts, etc. Jerry and Craig had showed up in tow.

I knew Jerry. I had kicked him off our Facebook group a couple of weeks before that, because I could tell he was just trying to co-opt and corrupt the group. Jerry would effusively agree with me via email that bankruptcy rights needed to be returned to student loans. When I challenged him to say it publicly, however, he wouldn’t do it. So that was the end of my relationship with the guy. His dis-ingenuity was easy to spot.

But there he was at Zuccotti Park, cheerleading for the Debt Collective. I could see $$ signs in both of their eyes.

When I realized it was Jerry Ashton’s hand I was shaking as he talked me up, I recoiled. After a very awkward conversation, Jerry literally shoved around $50 in cash into my pocket and they darted off as The Debt Collective put on their production, then left the park. I never saw them there again.

I immediately took the money from my pocket and gave it to the first ACTUAL activist on the park that I saw. The whole thing was just…gross.

It turns out that Jerry and Craig actually founded the Debt Collective’s “Rolling Jubilee” debt buyback gimmick, along with a related (similarly useless) initiative to purchase medical debt. The amount of money they are apparently bringing into these is huge. They are marketing both of these as a great relief for people, when in fact they are just a money-making scams to fund themselves as they pursue their much larger goal of a mass default.

Today, now that Debt Collective has realized its mass default, and its collection industry partners will be feasting, they pretend that they’ve been FOR bankruptcy rights all along.

I truly hope that people reading this will be smarter than that, and call them out for the very real damage they have caused, and the incalculable harms that are about to be inflicted on tens of millions of student loan borrowers everywhere by their despicable predatory business partners.

2. Student Debt Crisis.

This group used to be called “Cancel Student Debt to Stimulate the Economy”. They came around in 2009, started by a guy called Robert Appelbaum, a New York Lawyer.

Like the Debt Collective, SDC has disparaged the return of bankruptcy rights to student loans or remained silent on the issue. The unique feature of this group, today, is that they blatantly use their group has “hunting grounds” for distressed borrowers where they (or their industry partners who call themselves “Student Loan Lawyers”, and other names) steer these people into very expensive loan rehabilitation, consolidation, or other avenues where they can make very large commissions and fees from the transactions- probably without the borrowers even being made aware of how these “student loan lawyers”, and others are profiting from their debt.

The group came seemingly out of nowhere, grew explosively, claiming to be fighting for student loan cancellation. Like the Debt Collective, they were suspiciously silent on the bankruptcy issue, and in fact went to great lengths to kill the push for the return of this leverage to student loans.

Their activities included people like Rae Ann Roca (one of their admins) coming into our group, and very surreptitiously attempting to convince our members to abandon the push for bankruptcy protections. Rae Ann, and others in the group repeatedly used the argument that bankruptcy was unpleasant, and cancellation was much better…(precisely the same argument that Debt Collective operative would use a few years later).

This was all very weird to us. Some of our members looked into Appelbaum’s group, and found that Rae Ann Roca had come from the “war room” of the DCI Group, a DC lobbying firm known for creating fake grassroots groups on behalf of banks, Tobacco Companies, Oil Companies, etc. The DCI Group is credited with orchestrating a stealth lobbying campaign that killed legislation which would have prevented the sub-prime home mortgage crisis, for example.

Around the same time that we discovered this connection to the DCI Group, I received a “come on” from someone proposing a “joint venture”. His business was in coercing defaulted student loan borrowers into loan “rehabilitation”. This is where people with defaulted loans can get their loans out of default by paying for ten months (none of which goes to the loan), and then signing for a new, much larger loan. This rehabilitation is terrible. About 80% of these loans wind up in default again. But they are EXTREMELY lucrative for the agents who do this- they can get a 16% commission (of the value of the new, much larger loan). He told me that he already had a joint venture with Robert Appelbaum, the founder of the Forgive Student Debt group!

We asked Robert about this. He launched into a vulgar tirade that made very little sense. He accused me of being jealous that they had found a way to make money, and made some threatening statements about how I shouldn’t “poke the bear”, etc. I never had any contact with Robert after that.

Shortly thereafter, the admin (Rae Ann Roca), and Appelbaum both disappeared. Rae Ann went on to join a group called “The Young Invincibles”. Applebaum’s group then changed their name to “Student Debt Crisis”, and have been hanging around ever since. As best as I can tell, they use their group as hunting grounds where “debt coaches”, “Student Loan Lawyers”, and other hustlers hang out, preying upon defaulted borrowers, roping them into loan rehabilitation, or other schemes where they can make a TON of money- through commissions- at the great expense of the borrowers they rope into such arrangements, likely without their knowledge (“rehabilitated loans” default again around 80% of the time).

The legislation that the group has championed in the past, like HR. 4170, has put forth an absurd loan forgiveness plan (with no meaningful funding source) wrapped around what I can only call a massive bailout to the private student loan companies. HR. 4170, for example, called for the government to pay private student loan companies MORE THAN FULL-BOOK-VALUE for their private loans, many (perhaps most) of which would never have been worth 25 cents on the dollar on the market, in all likelihood.

One interesting aside: We did significant work on HR. 4170, and worked closely with Congressman Hansen Clarke’s staff, who sponsored/introduced the bill. We were asked by Clarke’s staff to write the bankruptcy related portion of the legislation. After we submitted the final draft to them- having been assured that it would be in the bill, Hansen’s staffer suddenly ceased all communications with us. When the bill finally came out a week or so later, every bit of the language about bankruptcy had been removed. The staffer we were working with literally disappeared, left Clarke’s staff, and to this day we have no idea what happened there. I suspect strongly that his removal from the staff, and the removal of bankruptcy language from the bill had something to do with the Student Debt Crisis people. The private lender bailout language they were championing definitely made it into the bill.

The last conversation I recall having with Natalia Abrams on this topic (somewhere around 2011), she was attempting to persuade me that the private student loan companies deserved to be paid more than full book value for their terrible, non-performing private loans.

So if I had to venture a guess, I would say that they are clearly a “front group”, actually doing the bidding of the private student loan industry, perhaps under direction from- or in cooperation with the DCI Group. Sickening Group. They seem to have duped MoveOn.Org, Elizabeth Warren, Chuck Schumer and many others. We will have nothing to do with them.

Both of these groups have been tellingly silent on returning bankruptcy rights for many years, and viciously opposed it (both publicly, and behind the scenes) People need to wake up to these dark forces.

I write this note because today, with the “on-ramp to repayment” now expired, the collection industry has free reign to pursue defaulted/delinquent borrowers viciously, and the non-payment rate for federal student loans is now well over 80%, in fact it is now closer to 90%.

The debt collection industry’s wildest dream has come true. We are now in the “mass default” that the Debt Collective has wanted since 2013, and bankruptcy rights remain gone from the loans. The Debt Collective are surely rejoicing.

The people at Student Debt Crisis, who use their group to target defaulted borrowers to convince to “rehabilitate” their loans (which is massively profitable for those who do the convincing, but massively harmful for 80% of the people who they convince, and will re-default on their loans), are surely also clinking the champagne glasses.

But the people who they misled, and tens of millions of borrowers across the country will be suffer.

It will be get brutal for defaulted student loan borrowers, and the number of defaults- will easily double in the coming months, if not triple.

Both of these groups are poised for massive growth as we go forward. They will surely see greatly increased influxes of funding, and inject even more distractive noise into the student loan space which will inevitably sew further Congressional and Presidential inaction, half-hearted actions, confusion, and ultimately, the perpetuation of this unconstitutional, nationally threatening, predatory loan scam.

I hope all the normal, distressed student loan borrowers out there will see these front groups for what they are, and turn away from them. Only StudentLoanJustice.Org and a handful of smaller grassroots groups (and even individuals) out there are can I confidently say are actually doing good work, fighting a good fight, and aren’t corrupted. They are very few and far between, hard to find amid all the Astroturf noise/propaganda, and constantly in danger of being drowned out completely by the industry and its adjuncts in this space.

Please stick with them.

Don’t let yourself be fooled anymore. The real cost/harm has already been too high, and promises to be far, far higher as this predatory loan scam perpetuates forward.